Public Limited Company Registration in India: A Foreign Investor’s Complete Guide for 2026

- June 27, 2026

- Posted by: admin-dlc

- Category: Uncategorized

Imagine you are a foreign business standing at the doorway of the world’s fourth-largest economy, a market of over a billion people that pulled in more than USD 81 billion of foreign direct investment in a single year. You want more than a quiet local presence — you want a vehicle that can raise serious capital, command the trust of banks and institutions, and one day, perhaps, ring the bell at a stock exchange. That vehicle is a public limited company, and registering one is the moment your India ambition stops being a plan and becomes a legal reality.

A public limited company (PLC) sits at the most ambitious end of India’s entry-structure spectrum. Unlike a private company, it can welcome an unlimited number of shareholders, its shares move freely, and it is purpose-built to access public capital. But that power comes with heavier responsibility — seven shareholders, three directors, stricter governance, and disclosure obligations that a private company never faces. For a foreign investor, the difference between a smooth incorporation and a stalled one comes down to understanding the rules before filing a single form. This guide takes you through the entire journey, in sequence, so that by the end you will know exactly what a PLC is, who can register one, how the process unfolds step by step, what it costs, and what happens after the certificate lands in your inbox.

1. What Is a Public Limited Company in India?

A public limited company is a business entity incorporated under the Companies Act, 2013 whose shares can be offered to the general public and are freely transferable without restriction. Its defining marker is its name: it ends simply in “Limited” — not “Private Limited.” Where a private company is a closed circle that caps its membership at 200 and restricts who can buy or sell shares, a public company is built to be open. It can have an unlimited number of shareholders, and ownership can change hands freely, whether the shares are privately held or eventually traded on an exchange like the NSE or BSE.

Three characteristics define the structure. First, it is a separate legal entity: the company exists independently of the people who own and run it, can hold property, and can sue and be sued in its own name. Second, it offers limited liability: a shareholder’s exposure is capped at the unpaid amount on their shares, so personal assets are shielded from the company’s debts. Third, it enjoys perpetual succession: the company continues regardless of changes in its directors or shareholders, surviving the people who created it. For a foreign investor entering an unfamiliar market, this combination of legal separateness and durability is precisely what makes the company form attractive.

It is worth clearing up a common confusion early. A public company is not the same as a listed company. Every listed company is public, but not every public company is listed. A foreign-owned PLC can remain unlisted for years — using the structure purely for its governance credibility, its capacity to take on many shareholders, and its readiness to raise public capital when the time is right. Registration as a PLC does not force you to go public immediately; it simply keeps that door open. Indian companies such as Meesho Limited adopted the public structure well before any IPO ambitions matured, precisely because the form gives you optionality.

2. Why Foreign Investors Choose a Public Limited Company

If a private limited company is simpler and cheaper to run, why would a foreign investor take on the heavier PLC? The answer is ambition. The PLC is engineered for businesses that intend to grow large and raise capital at scale, and it offers advantages that a private structure simply cannot match.

The headline benefit is fundraising power. A public company can raise money directly from the public by issuing shares through a prospectus — an option closed to private companies. This unlocks access to a far larger pool of capital and makes it easier to attract the large institutional investments that fuel rapid growth. For a foreign business with serious expansion plans, this capacity to tap public markets later is a strategic asset worth securing at incorporation.

Close behind is credibility and trust. Public companies are subject to stricter governance and disclosure requirements, and that transparency is precisely why customers, lenders, and institutional investors instinctively trust them. When a foreign-owned company can show audited accounts, a proper board, and public disclosure, it signals seriousness in a way that opens doors — to bank credit, to partnerships, and to investor confidence. Add to this share liquidity (shares transfer freely, without needing other shareholders’ approval) and perpetual succession, and the PLC becomes the natural home for a venture that sees itself as a long-term, large-scale player rather than a closely held operation.

None of this means the PLC is right for everyone. For a single foreign owner who wants tight control of a modest India operation, a wholly-owned subsidiary (a private limited company) is usually simpler and cheaper. The PLC earns its place when the plan genuinely involves many shareholders, public fundraising, or a future listing. Choosing between them is the first strategic decision a foreign investor makes — and it should be made deliberately, with the growth plan firmly in view.

Public limited vs other entry structures — a quick comparison

Before committing to a public company, it helps to see how it sits against the other vehicles a foreign investor can use to enter India. The table below summarises the practical differences.

| Feature | Public Ltd | Private Ltd / WOS | LLP | Branch / Liaison |

|---|---|---|---|---|

| Min. shareholders / partners | 7 | 2 | 2 partners | N/A (extension of parent) |

| Min. directors | 3 | 2 | 2 partners | Authorised rep. |

| Resident Indian needed | Yes (1 director) | Yes (1 director) | Yes (1 partner) | Yes (signatory) |

| Raise capital from public | Yes | No | No | No |

| 100% FDI, automatic route | Most sectors | Most sectors | Most sectors* | RBI approval |

| Permitted activities | Full commercial | Full commercial | Full commercial | Restricted |

| Compliance burden | Highest | Moderate | Lower | Moderate |

| Best for | Scale & future IPO | Wholly-owned control | Services, lean setup | Representative presence |

3. Who Can Register: Eligibility & FDI Rules for Foreigners

The reassuring headline for international businesses is that India actively welcomes foreign ownership of public companies. Foreign nationals, NRIs, and foreign corporate entities can all be shareholders and directors, and the Companies Act expressly permits non-residents to serve as directors. There is no requirement that shareholders be resident in India. This openness is exactly why the public and private limited company are the two preferred vehicles for foreign investment into India.

To register, a foreign founder must satisfy a handful of core conditions:

- Seven shareholders. A public company needs at least seven members (subscribers to the MoA), with no upper limit. Each of the seven must take at least one share and sign the Memorandum before a witness. These can be a mix of foreign individuals, the foreign parent company, and trusted nominees to meet the count.

- Three directors. A minimum of three directors is required, each holding a valid Director Identification Number (DIN). At least one director must be resident in India — defined under Section 149(3) as having stayed in India for at least 182 days in the immediately preceding financial year. The other directors can be foreign nationals based abroad.

- A registered office in India. A physical address in India is mandatory before incorporation and becomes a public record on the MCA portal.

- A compliant name. The name must end in “Limited,” follow MCA naming rules, and not clash with an existing company or trademark.

Foreign investment itself is governed by the Foreign Exchange Management Act (FEMA) and India’s FDI policy, which runs on two routes. Under the automatic route, no prior government approval is needed — the investor simply files post-investment reports with the RBI. As of 2025-26, over 90% of sectors permit 100% FDI under this route, covering most technology, services, and manufacturing activities. Under the government (approval) route, sensitive sectors face caps or require clearance.

| Sector (illustrative) | FDI cap | Route |

|---|---|---|

| Most manufacturing, IT & software, B2B e-commerce | 100% | Automatic |

| Defence | Up to 74% | Automatic; beyond 74% by government approval |

| Insurance | Up to 74% | Automatic |

| Multi-brand retail trading | 51% | Government |

| Print & broadcasting media | 26%–49% (activity-specific) | Government |

| Lottery, gambling, atomic energy, tobacco mfg. | Prohibited | Not permitted |

4. Step-by-Step: The Registration Process

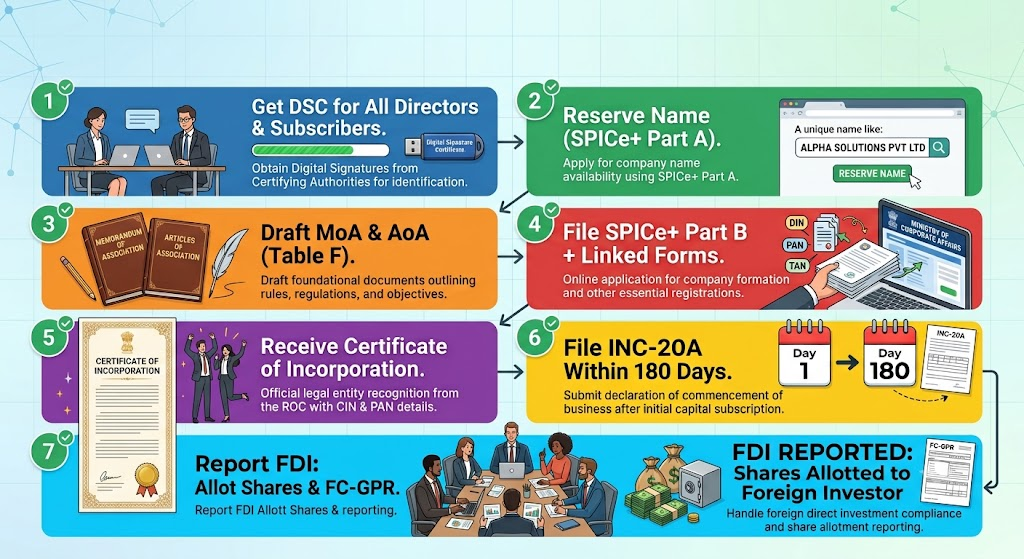

India has digitised company incorporation through the SPICe+ (Simplified Proforma for Incorporating Company Electronically Plus) web form on the MCA portal — a single-window application that bundles name reservation, DIN, incorporation, PAN, TAN, and more into one process. Here is the journey from zero to a fully registered, operational public limited company, in sequence.

- Obtain Digital Signature Certificates (DSC). Every proposed director and subscriber needs a Class 3 DSC to sign incorporation documents electronically. Foreign directors obtain theirs using a passport and notarised/apostilled identity and address proof. This is the foundation — nothing can be filed without it.

- Reserve the company name (SPICe+ Part A). Submit up to two proposed names with the relevant activity code. The name must end in “Limited” and not conflict with an existing company or trademark. If both names are rejected, you get one free resubmission; beyond that, a fresh filing and fee apply. An approved name stays valid for a limited window, so proceed promptly.

- Draft the MoA and AoA. The Memorandum of Association (filed as Form INC-33) defines the company’s objects, registered-office state, liability, and capital; the Articles of Association (Form INC-34) set the internal rules — share transfers, board meetings, voting, dividends. Public companies typically adopt rules aligned with Table F of the Act. All seven subscribers sign these before a witness.

- File SPICe+ Part B with linked forms. Complete the main incorporation data and attach the MoA, AoA, and declarations. DIN can be allotted within SPICe+ for up to three directors; if more directors need DINs at incorporation, the extras apply separately via Form DIR-3 (or are appointed later). Linked forms — AGILE-PRO (for GST, EPFO, ESIC, bank account), INC-9 declarations, and DIR-2 consents — are auto-populated, downloaded as PDFs, and digitally signed. A practising professional certifies the filing.

- Receive the Certificate of Incorporation (COI). Once the Registrar of Companies is satisfied, it issues the COI with the company’s Corporate Identity Number (CIN), along with PAN and TAN. Your company now legally exists.

- File Form INC-20A within 180 days. Before it can commence business or exercise borrowing powers, the company must file the declaration of commencement of business (INC-20A) within 180 days of incorporation, confirming that subscribers have paid for their shares. This step is easy to forget and carries penalties if missed.

- Report the foreign investment. When foreign capital reaches the company’s Indian bank account, shares must be allotted within 60 days, and the investment reported to the RBI through the FIRMS portal (FC-GPR). Setting up this reporting calendar immediately avoids penalties.

With clean, correctly attested documents and no sector-specific clearances, this entire sequence typically completes in about 15–21 working days. The slowest variable for foreign founders is rarely the MCA’s processing — it is the time taken to notarise and apostille documents abroad, which is why that preparation should start early.

5. Documents You Will Need

Document preparation is where foreign incorporations most often slow down, because papers executed abroad usually need notarisation and apostille (or consular legalisation) before India accepts them. Names and addresses must match exactly across every document — even a minor spelling variation can trigger rejection. The requirements fall into three groups.

For foreign directors & shareholders (individuals)

- Passport copy (mandatory identity proof for foreign nationals), notarised and apostilled.

- Address proof — recent bank statement, utility bill, or driving licence — notarised/apostilled and within the accepted age limit.

- Recent passport-size photograph.

- Consent and declaration forms (DIR-2, INC-9), signed using the DSC.

- Class 3 Digital Signature Certificate for each director and subscriber.

For a foreign corporate shareholder (the parent company)

- Board resolution authorising the investment and naming an authorised signatory.

- Certificate of incorporation and charter documents of the parent, apostilled.

- KYC extending up the ownership chain to the ultimate beneficial owner.

For the company & registered office

- MoA (INC-33) and AoA (INC-34) defining objects and internal governance.

- Proof of registered office — rent/lease agreement or sale deed.

- No-objection certificate (NOC) from the property owner if the premises are rented.

- A recent utility bill (electricity, water, or gas), generally not older than two months.

Prepare banking KYC in parallel. Authorised dealer (AD) banks separately require detailed KYC for the foreign investor — identity, address, beneficial-ownership declarations, and source-of-funds documentation, following the chain to the ultimate beneficial owner. Getting this ready alongside the MCA filings prevents the classic bottleneck where a company is incorporated but cannot operate because its account and FDI inflow are stuck on paperwork.

6. Capital, Costs, Timeline & Taxation

A welcome surprise for many foreign investors is that there is no mandatory minimum paid-up capital for a public limited company in most sectors. The old Rs. 5 lakh requirement was removed by the Companies (Amendment) Act, 2015. In practice, banks expect a reasonable opening balance to operate a corporate account, and you choose an authorised capital figure appropriate to the business — higher authorised capital simply means proportionally higher MCA filing fees and stamp duty.

| Component | What to expect |

|---|---|

| MCA / SPICe+ filing fee | Varies with authorised capital |

| Stamp duty on MoA & AoA | Varies by state |

| DSC (per director/subscriber) | Roughly Rs. 800–2,000 each |

| Name reservation | ~Rs. 1,000 |

| Professional fees (CA/CS) | Commonly Rs. 5,000–15,000+ |

| PAN & TAN | Included in SPICe+ |

| Typical total | ~Rs. 15,000–40,000+ (plus overseas legalisation for foreign founders) |

| Timeline | ~15–21 working days with complete documents |

On taxation, a company incorporated in India is taxed as a domestic company on its income, while a foreign company operating through a branch is generally taxed only on India-sourced income but at a higher corporate rate. This is a key reason foreign groups usually prefer incorporating an Indian company over running a branch — the Indian company is a separate legal entity with its own tax identity, clearer compliance, and full access to the domestic market. India’s network of Double Taxation Avoidance Agreements (DTAAs) can further reduce tax on cross-border flows such as dividends, so the structure should be reviewed alongside your home-country tax position. GST registration becomes mandatory only once the business crosses the applicable turnover threshold or its activity requires it.

| Entity / regime | Headline corporate tax rate* |

|---|---|

| Domestic company — concessional regime (Sec. 115BAA) | 22% + surcharge & cess (≈25.17% effective) |

| New domestic manufacturing company (Sec. 115BAB) | 15% + surcharge & cess (≈17.16% effective) |

| Domestic company — older regime (turnover-based) | 25% or 30% + surcharge & cess |

| Foreign company branch (India-sourced income) | ≈35% + surcharge & cess |

*Indicative rates for AY 2026-27; surcharge varies with income, plus 4% health & education cess. Concessional regimes carry conditions. Confirm current rates and eligibility with a tax advisor. This shows concretely why an Indian company is usually more tax-efficient than a branch — and why DTAAs matter for repatriation.

7. Life After Incorporation: Ongoing Compliance

Receiving the Certificate of Incorporation is the beginning, not the end. A public company carries heavier ongoing compliance than a private one, and for a foreign-funded company the FEMA layer adds further obligations. Treating these as routine — and diarising them from day one — is what keeps the company in good standing.

The core recurring obligations include the INC-20A commencement filing within 180 days; regular board and general meetings; a mandatory statutory audit of accounts regardless of size; and annual filings with the Registrar of Companies (annual return and financial statements) within prescribed timelines. Directors must keep their KYC current, and statutory registers must be maintained. On the foreign-investment side, the company must complete FC-GPR reporting after allotting shares to foreign investors and file the annual Foreign Liabilities and Assets (FLA) return with the RBI each year. Public companies also face stricter disclosure norms and, if they ever list, additional SEBI compliance.

The thread here is simple: the obligations are manageable when planned for, but they are not optional. The cost of ignoring post-registration compliance — penalties, disqualifications, and problems in future due diligence — almost always exceeds the cost of doing it properly. Many foreign investors engage a local advisor or virtual CFO to own the compliance calendar, which is consistently cheaper than remediation later.

Key post-incorporation compliance calendar

The following deadlines are the ones foreign-funded public companies most often need to diarise. Dates and penalties below are indicative for 2026 and should be confirmed for your specific facts.

| Obligation | Deadline | Note if missed |

|---|---|---|

| Allotment of shares to foreign investor | Within 60 days of funds reaching the account | FEMA violation; compounding required |

| FC-GPR (report FDI on RBI FIRMS portal) | Within 30 days of share allotment | Late fee (LSF) plus possible penalty |

| INC-20A (commencement of business) | Within 180 days of incorporation | Penalty on company & officers; bars operations |

| First auditor appointment | Within 30 days of incorporation | Board, then members, must appoint |

| FLA return (Foreign Liabilities & Assets, to RBI) | By 15 July each year | Required of every company holding FDI |

| DIR-3 KYC (for each director with a DIN) | By 30 September each year | DIN deactivated; Rs. 5,000 reactivation fee |

| Annual ROC filings (AOC-4, MGT-7) & AGM | AGM within 6 months of year-end; filings thereafter | Daily late fees per form |

Indicative for 2026. FC-GPR late submission attracts a Late Submission Fee and, in some cases, penalties under FEMA; ROC forms attract per-day additional fees. Confirm current timelines and amounts with your advisor.

8. Common Mistakes Foreign Investors Should Avoid

Most problems in foreign setups are not caused by the law being hard — they are caused by avoidable errors at the planning and filing stage. Knowing them in advance is the simplest way to keep your incorporation smooth.

- Choosing the wrong structure. Defaulting to a public company when a private limited company or wholly-owned subsidiary would have been simpler and cheaper to run. The PLC’s heavier compliance is only worth it if you genuinely expect many shareholders or public fundraising.

- Ignoring sector-specific FDI limits. Assuming 100% automatic-route ownership applies when the activity sits under a cap or the approval route. Verify before filing.

- Underestimating document legalisation. Forgetting that documents signed abroad need notarisation and apostille, then watching the timeline slip while papers are re-executed.

- Mismatched registered-office documents. Tiny inconsistencies between the rent agreement, NOC, and utility bill trigger MCA rejection. Match names and addresses exactly.

- Missing INC-20A. Failing to file the commencement-of-business declaration within 180 days, which blocks operations and attracts penalties.

- Missing the 60-day allotment / FDI reporting. Not allotting shares within 60 days of the foreign inflow, or skipping FC-GPR and the annual FLA return, leading to FEMA penalties.

- Treating compliance as one-time. Cheap incorporation without an ongoing compliance plan becomes expensive later. Set up the calendar on day one.

The thread running through every one of these is the same: the law in 2026 is genuinely investor-friendly, but it rewards discipline. Plan the structure, verify the FDI route, prepare documents carefully, and respect the post-registration calendar. Foreign investors who do this consistently report a fast, clean entry into the Indian market.

Frequently Asked Questions (FAQ)

Can a foreigner or NRI register a public limited company in India?

Yes. Foreign nationals, NRIs, and foreign companies can be shareholders and directors. The company needs at least seven shareholders and three directors, and at least one director must be resident in India (182+ days in the preceding financial year).

How many shareholders and directors are required?

A minimum of seven shareholders and three directors, with no upper limit on shareholders. Each of the seven initial subscribers must take at least one share and sign the MoA before a witness.

Is there a minimum capital requirement?

There is no mandatory minimum paid-up capital in most sectors — the Rs. 5 lakh requirement for public companies was removed by the Companies (Amendment) Act, 2015. Banks, however, expect a reasonable opening balance, and you set an authorised capital based on business needs.

How long does registration take?

Typically about 15–21 working days with complete, correctly attested documents and no sector clearances. For foreign founders, the main variable is the time to notarise and apostille documents abroad.

What does it cost to register a public limited company?

Costs combine MCA filing fees (vary by authorised capital), state stamp duty on MoA/AoA, DSC charges per person, name reservation, and professional fees — commonly in the range of roughly Rs. 15,000 to Rs. 40,000 or more, plus document-legalisation costs for foreign founders. Treat any single figure as indicative.

Can the whole process be done online?

Yes. Registration is completed online through the MCA portal using the integrated SPICe+ web form, which bundles name reservation, DIN, incorporation, PAN, TAN, and other registrations into one application.

What is the difference between a public and a private limited company?

A public company needs seven shareholders and three directors, can offer shares to the public, and has freely transferable shares; a private company needs two shareholders and two directors, caps membership at 200, and restricts transfers. A public company also faces stricter governance and disclosure norms.

Does a public limited company have to list on a stock exchange?

No. Every listed company is public, but not every public company is listed. Many foreign-owned public companies stay unlisted for years, using the structure for credibility and the option to raise public capital later.

Do foreign shareholders need RBI approval to invest?

In most sectors, no — over 90% of sectors permit 100% FDI under the automatic route, requiring only post-investment reporting to the RBI. Sensitive sectors (e.g. defence, insurance, multi-brand retail, media) have caps or need government approval, so confirm your sector first.

What is Form INC-20A and why does it matter?

INC-20A is the declaration of commencement of business, which a company must file within 180 days of incorporation before it can begin operations or exercise borrowing powers. Missing it attracts penalties, so it should be diarised at incorporation.

What happens after the foreign investment arrives?

Shares must be allotted to the foreign investor within 60 days of the capital reaching the company’s Indian bank account, and the investment must be reported to the RBI through the FIRMS portal (FC-GPR). Late reporting attracts penalties.

What are the main ongoing compliance obligations?

A public company must hold board and general meetings, get its accounts audited, file annual returns and financial statements with the ROC, and — if foreign-funded — file FEMA-related returns such as the annual FLA return. Public companies face heavier compliance than private ones.

Ready to Register Your Public Limited Company in India?

Delhi Legal Company helps foreign investors set up public and private limited companies end-to-end — SPICe+ incorporation, resident director and registered office services, FDI/FEMA reporting, and ongoing compliance. Let us make your India entry simple and fully compliant.

☎ +91-9599332456 ✉ info@delhilegalcompany.com 🌐 delhilegalcompany.com